Before the first truck rolls, before the first flotation cell turns, Sierra Gorda’s challenge is already in motion.

It begins 143 kilometres away, at Mejillones on Chile’s northern coast, where seawater starts a long engineered journey inland. From there it moves into one of the driest mining environments on Earth, toward a copper operation that was never going to win on grade alone. Sierra Gorda, deep in the Atacama Desert, does not have that luxury. Its orebody is low grade. Its margins depend on control. Its future depends on whether infrastructure, process discipline and expansion logic can keep moving in step.

That is what makes Sierra Gorda SCM worth watching.

In an industry still drawn to the scale and spectacle of new-build megaprojects, Sierra Gorda has been advancing in a different way: by forcing more value out of what is already there. The open-pit Catabela operation, a 55-45 joint venture between KGHM Polska Miedź S.A. and South32, began commercial production in 2015 as a 110,000-tonnes-per-day Phase I plant built to treat low-grade porphyry ore. By 2024, the site was routinely processing about 49 Mtpa, roughly 30% above its original design basis. That gain did not come from a fresh multibillion-dollar build. It came from de-bottlenecking, equipment changes, better process control and the kind of brownfield discipline that rarely looks glamorous from the outside.

Yet this is exactly the sort of work that will define much of the next generation of copper supply.

In 2024, Sierra Gorda produced 154,559 tonnes of copper and 2,808 tonnes of molybdenum. Its annual power demand — roughly 1,310 GWh — is supplied through a long-term renewable power purchase agreement with AES Andes. Its process water comes from seawater, not continental freshwater, delivered through that dedicated Mejillones pipeline. By the end of 2025, KGHM had revalued its stake in the mine at US$504 million after the repayment of nearly US$1 billion in liabilities between 2021 and 2025. On a 100% basis, the operation generated US$1.48 billion in revenue and US$291 million in net profit in the first nine months of 2025.

Those are headline numbers. But the deeper story is not about one year’s performance. It is about how a difficult asset was made more resilient, more expandable and more relevant at a time when copper projects are becoming harder to permit, harder to fund and harder to operate.

A Mine Built on Constraint

Sierra Gorda’s copper grade is about half the Chilean national average. That shapes everything.

Low-grade mining narrows the operating window. It makes energy efficiency more important. It makes recovery stability more important. It makes downtime more expensive. A high-grade mine can hide certain inefficiencies for longer. A low-grade one cannot. The engineering must be tighter. The interfaces between mine planning, grinding, flotation, tailings handling and maintenance must hold.

That is why Sierra Gorda’s progress reads less like a breakthrough and more like a sequence of technical decisions, each one adding a little more room to an otherwise unforgiving system.

The 2024 throughput record came through that accumulation. Engineers added a third tailings thickener and a fourth concentrate filter. They modified shear agitation tanks. They upgraded pumps and conveyors. High-pressure grinding rolls were introduced to improve comminution efficiency and reduce energy intensity. Process controls were refined to support more consistent Cu-Mo flotation performance under changing ore conditions. None of this is theatrical. All of it matters.

That is often how brownfield value is created: not in one dramatic act, but in a long succession of improvements that make a plant steadier, faster and harder to interrupt.

Marcelo Bustos Collao, who became CEO on 1 July 2025, arrived with operating experience shaped in Chilean mining rather than in boardroom abstraction. A mining civil engineer and extractive metallurgist trained at the University of Chile, with a background spanning Carmen de Andacollo, Teck Chile, Los Bronces and El Soldado, Bustos stepped into Sierra Gorda with a clear reading of the asset. It is low grade, yes, but it is also highly capable — provided the operation keeps tightening the system around it.

He has framed that direction around three pillars: Unique Culture, Operational Excellence and Responsible Mining. At Sierra Gorda, those ideas are not especially interesting as slogans. They become interesting only when they appear in plant performance, infrastructure decisions and workforce execution.

And that is where the mine has been making its case.

The Real Asset Is the System Around the Plant

Copper operations are often described by their reserves, grades and annual output. Those metrics matter. But at Sierra Gorda, the more revealing story sits in the enabling system around the concentrator.

In northern Chile, water and power are never incidental. They are strategic. They affect cost, permitting, expansion pathways and long-term risk. A mine that secures them well is not just better supplied. It is better positioned.

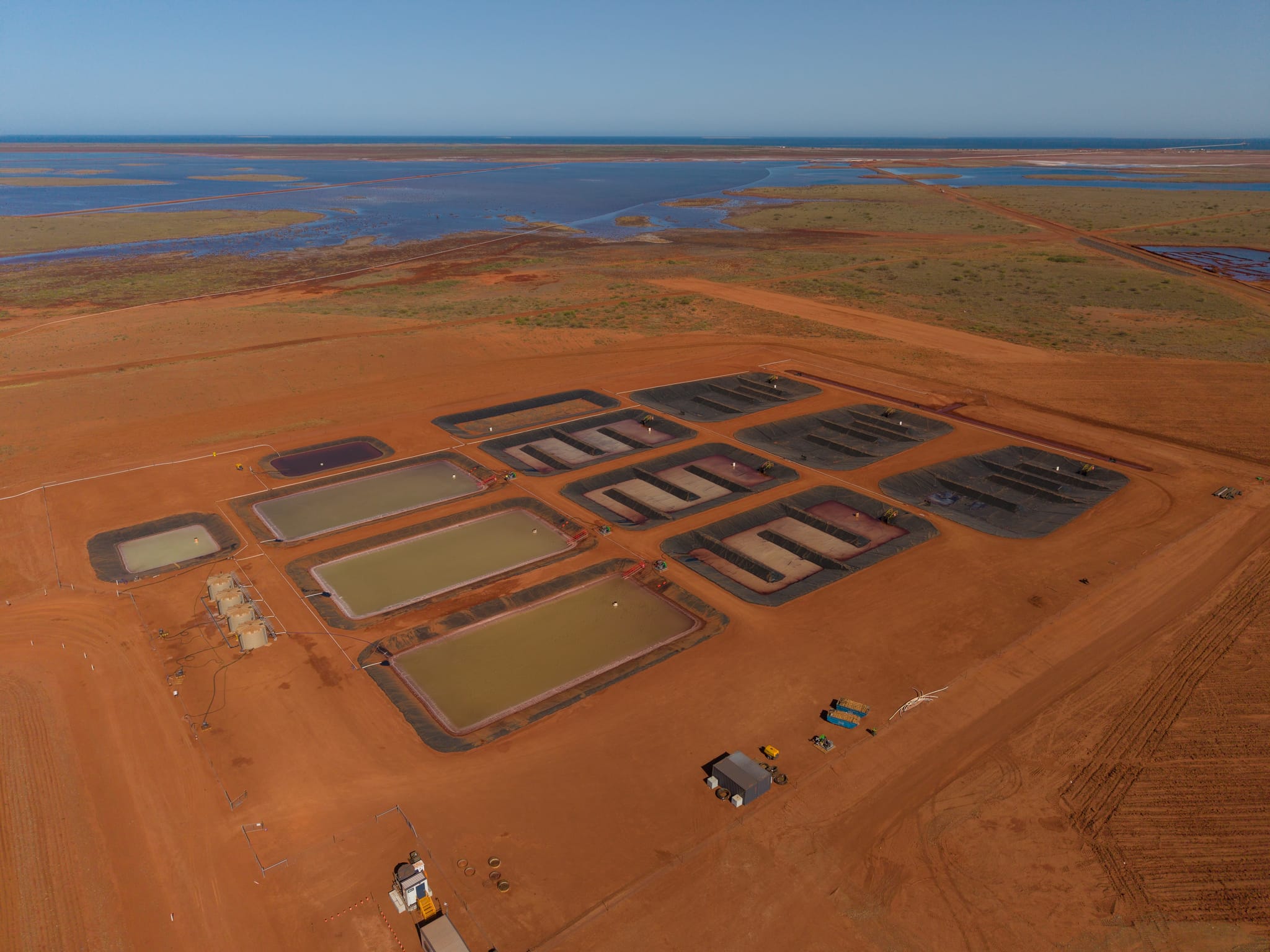

Sierra Gorda’s seawater system is a case in point. Process water is supplied through a 143-kilometre dedicated pipeline from Mejillones, allowing the operation to function without continental freshwater. Less than 10% of that water is desalinated, mainly for the molybdenum plant and camp. The rest supports the broader process circuit. With the addition of the third tailings thickener pushing densities above 60%, recirculation has improved further, helping close the loop in a region where every water decision carries operational and political weight.

The power arrangement works in the same strategic way. Sierra Gorda’s energy demand is covered under a long-term renewable agreement with AES Andes, drawing on a mix of solar, wind, hydro and storage-backed supply. In another context, this might be written off as an ESG talking point. Here it is something more practical. It lowers emissions, yes, but it also stabilises a large power-intensive industrial system in a region where long-term energy planning shapes competitiveness.

Together, those two infrastructure lines — water and power — do more than support current production. They change the mine’s future options.

That becomes especially important when expansion comes back into view.

The Next Expansion Is Not Starting From Zero

When Sierra Gorda’s Phase I plant was originally delivered, expandability was built into the concept. At one point, the operation was expected to move toward a much larger Phase II development. That larger build was deferred. Instead, the owners took a slower route: improve the installed base, strengthen the economics, then expand from a position of greater control.

It now looks like a shrewd sequence.

The next step under evaluation is a fourth grinding line, along with additional flotation capacity and supporting infrastructure. The proposed expansion would lift throughput to around 58 Mtpa, another material increase. What makes it notable is not simply the volume gain, but the shape of the opportunity. Much of the hardest groundwork — the water line, the power framework, the site platform — is already there. That lowers capital intensity and reduces the risk profile compared with an equivalent standalone development.

This is where good infrastructure planning begins to reveal its second life. Extra capacity built in years ago can look expensive in the moment. Later, it becomes the reason a mine can expand at all without starting over.

Exploration is advancing alongside that brownfield pathway. Over the past two years, more than US$32 million has gone into drilling at the adjacent Catabela Northeast porphyry, which remains open in all directions. A JORC Exploration Target of 1.1–2.9 billion tonnes at 0.45–0.48% total copper points to mine-life extension potential that is meaningful in any copper market, and especially so in this one. An oxide stockpile of around 110 Mt is also being assessed for possible heap-leach/SX-EW treatment.

So Sierra Gorda’s future is not being shaped by one lever alone. It is being built through the overlap of three things: a stronger plant, an expandable infrastructure base and a reserve story that still has room to run.

Contractor Ecosystem: The Operating System Behind the Asset

Brownfield optimisation is often described in terms of plant upgrades and capital efficiency, but mines do not de-bottleneck themselves. Somewhere behind every throughput gain is a contractor, a maintenance team, a component supplier, a controls specialist, a logistics partner — usually many of them — keeping the system intact long after the capital slide has disappeared from view.

At Sierra Gorda, that ecosystem is both broad and increasingly strategic. The mine’s 148 local service providers and 192 goods suppliers accounted for roughly 29% of total spend in recent years. At the Connected Suppliers 2025: Sustainability Dimension event in Antofagasta, more than 100 contractors came together to tackle social, economic and environmental issues. Awards went to Puerto Angamos for its community programme and ROES Ecocir for circular-economy insulating panels made from textile waste and discarded mattresses.

VP Supply Chain Sandra Montiel Chamorro has embedded a 10–15% sustainability weighting into tender evaluations, a reminder that procurement at large industrial sites is no longer judged on price and delivery alone. The question now is not only whether suppliers can perform, but how they perform, and what kind of operating environment they help create around the mine.

That is particularly visible in the range of roles Sierra Gorda’s suppliers play. Macep Ltda. Chile provides industrial maintenance, metalworking, civil construction and on-site logistics that help keep both plant and mobile equipment functioning around the clock. Komatsu Chile S.A. supports the open-pit fleet, including 930E haul trucks, D475-A bulldozers, WD900-3 wheel dozers and GD825A motor graders. PROK Chile supplies conveyor idlers that are central to reliable material handling. Hatch delivered detailed engineering for the molybdenum plant, one of the site’s important process facilities. Busanc Sociedad Sances Limitada, recognised by Sierra Gorda at industry events, contributes specialised goods and support services. Sitrans LTDA provides instrumentation and control expertise essential to maintaining process reliability in the Cu-Mo concentrator.

The point is not simply that Sierra Gorda has many suppliers. Large mines do. The point is that, on a site like this, the contractor network is not an outer ring around the asset. It sits inside the asset’s performance. It influences uptime, plant stability, maintenance quality, response time and increasingly the site’s sustainability profile. At a low-grade operation, where inefficiency has less room to hide, that is not a supporting detail. It is part of the operating model.

ESG Here Is Not Decoration

Mining companies often describe ESG in language that floats a little too far above the site itself. Sierra Gorda is more persuasive when the focus stays on what has actually been built, changed or maintained.

The strongest examples are physical. Renewable electricity. Seawater infrastructure. Thickened tailings. These are not abstract commitments. They are engineered decisions with operational consequences. In a water-stressed desert environment, they also have a direct bearing on social licence.

Bustos has described sustainability as “respect for the territory, responsibility towards communities, innovation with purpose.” Sierra Gorda also speaks of itself as un vecino más — one more neighbour. That kind of phrase can sound easy in isolation. It becomes more credible only when backed by repeated local engagement and measurable programmes.

The Trainee Comunitario programme is one example. Now in its tenth year, it recruits local residents into a full year of paid technical and safety training at market wages, with successful graduates moving into permanent roles. Nearly 60 neighbours have already been integrated into the operation through the programme. In 2025, 20 new places were opened, with 13 apprentices joining the latest intake.

Health infrastructure has been another focus. In 2025, an ophthalmological campaign in Mejillones delivered more than 700 pairs of lenses, more than 400 in-person consultations and 125 complex evaluations through partnerships involving the municipality, the Community Hospital, the Antofagasta Health Service and Desafío Levantemos Chile. A telemedicine platform followed, giving local residents access to more than 20 medical specialists without long journeys to larger urban centres.

Then there is the kind of response that tells you how a company behaves when it is not speaking from a podium. After a late-2025 frontal system flooded parts of Sierra Gorda town, the company deployed crews and vacuum trucks for a two-day emergency street-cleaning operation. That voluntary effort has since continued on a three-times-per-week basis to help reduce suspended particulate matter on local roads.

In August 2025, Sierra Gorda formalised a broader environmental alliance with BHP’s Spence and Antofagasta Minerals’ Centinela through a territorial Clean Production Agreement focused on dust studies, mitigation measures and social investment to improve air quality in the commune. It was a practical move, and perhaps an inevitable one. In northern Chile, shared environmental pressures increasingly demand shared responses.

Why Sierra Gorda Matters Now

There is a wider reason Sierra Gorda deserves attention beyond its own production figures.

The copper market increasingly needs growth from places that are harder to build, harder to permit and harder to run. The next tranche of supply will not all come from clean-sheet discoveries with perfect grades and uncomplicated infrastructure corridors. Much of it will come from assets already in operation — assets that can be pushed further through engineering, better systems and smarter use of installed capacity.

That is where Sierra Gorda enters the conversation.

It shows what a low-grade copper operation can become when management stops treating grade as destiny and starts treating the asset as a systems problem. It shows what happens when water security is solved as infrastructure, not as an afterthought. It shows the advantage of expansion pathways built on existing power, process and logistics capacity rather than on entirely new footprints. And it shows why brownfield work, so often overshadowed by the mythology of the next big mine, may end up delivering some of the industry’s most meaningful tonnes.

Sierra Gorda is not finished proving itself. The fourth grinding line still needs a final investment decision. Exploration still needs to convert promise into longer-term certainty. Low-grade mining will remain operationally unforgiving. But the operation has already demonstrated something that matters far beyond northern Chile: in a constrained mining world, the smartest growth may not come from starting over. It may come from building more intelligently on what is already there.

At Sierra Gorda, that is no longer a theory. It is the operating reality.

DOWNLOAD

Seirra Gorda -Mine- Feature 2026.pdf

Seirra Gorda -Mine- Feature 2026.pdf