2010 has been a stellar year to date for Rockwell Diamonds Inc. CEO John Bristow talks to Jayne Flannery about the trends and factors moving in the company’s favour.

2009 was an awful year for the diamond industry, with markets recording an unprecedented plummet in prices of around 50 per cent. As the global recession hit, it seemed that diamonds were no one’s best friend. Girls the world over were finding themselves compelled to downgrade and weigh up cheaper options.

However, Rockwell Diamonds Inc. succeeded in weathering the storm better than most. As a junior player in South Africa’s mining industry, the company’s size and agility meant it could respond to the global downturn much more nimbly than some of its large and cumbersome competitors.

“We were able to react very quickly, particularly in cutting costs by placing our least viable mine at Wouterspan on a care and maintenance regime. At the same time, we made some tough but necessary business decisions and a range of operational enhancements to reduce our cost base. The processes we use are not unique, but we have a very large scale processing capability which enables us to achieve unprecedented economies of scale within the industry,” says John Bristow, CEO.

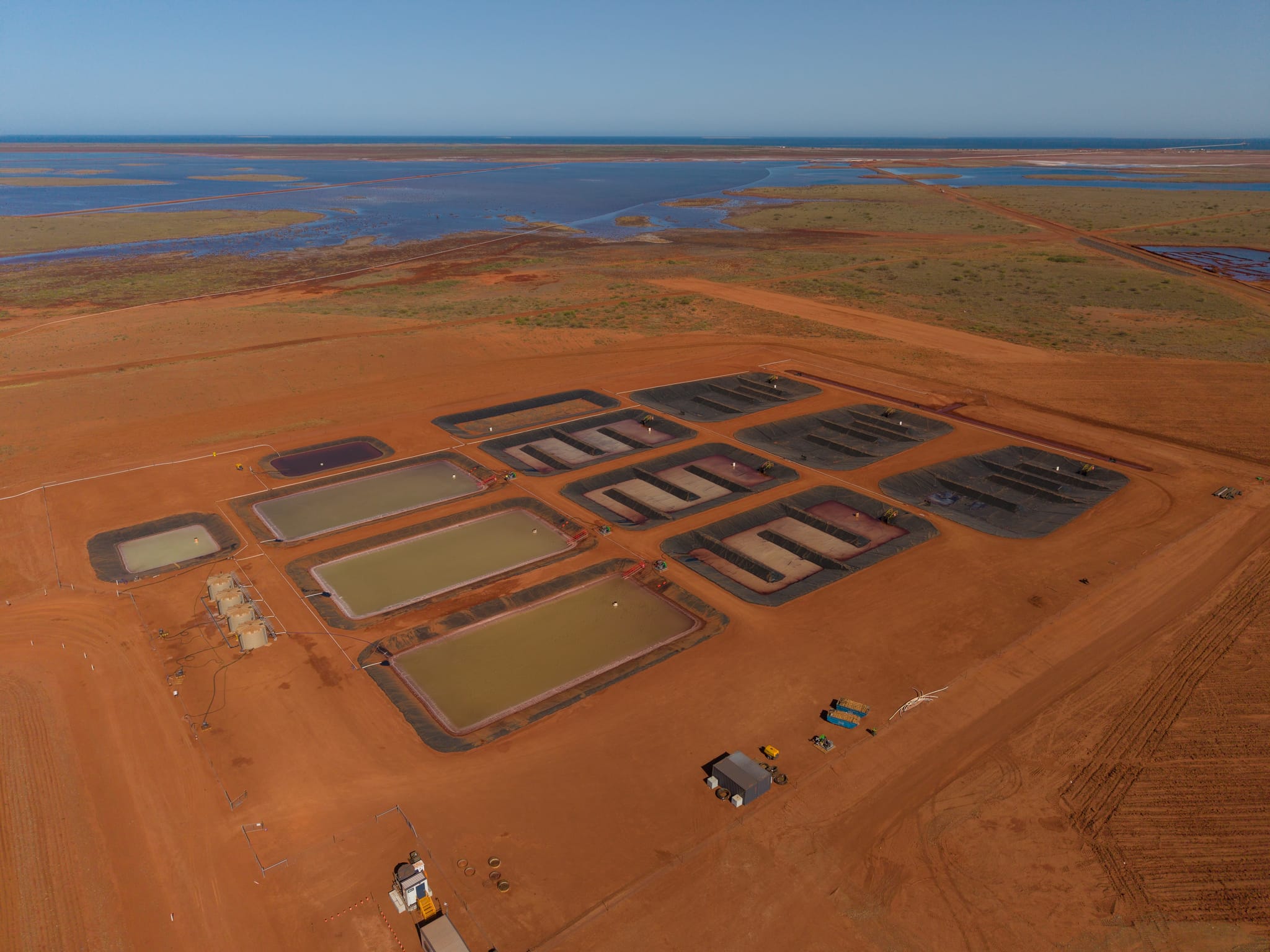

Like many junior players in South Africa’s mining industry, the company is listed on the Toronto Stock Exchange but its activities are wholly focused on South Africa’s alluvial deposits. Rockwell has diamond operations in the Northern Cape Province—the Holpan and Klipdam mines are located north of Kimberley, while the Saxendrift mine is on the Middle Orange River to the south-west of Kimberley. The company is currently engaged in a bulk sampling project at a hitherto unused extension of the Klipdam mine in the Northern Cape.

Most importantly Rockwell is also in the process of acquiring the Tirisano (or Blue Gum) operation of Etruscan Diamonds, located in the well-known Ventersdorp alluvial diamond district in South Africa's North West Province.

“We have now achieved a very large footprint in low grade alluvial deposits of exceptional diamonds. Our assets are particularly valuable because diamonds are becoming scarcer all the time, with no new viable discoveries made for a number of years,” Bristow says.

In all its operations, Rockwell uses open-cast or horizontal strip mining operations. This method of mining offers the lowest recovery costs of all—the key technical challenge is devising efficient processes to sift and process countless tonnes of rock and earth in order to extract a few precious gems. It is essentially a large earth moving and processing operation, which Rockwell has carefully refined and perfected.

Through a combination of innovation, a low cost structure and a focus on the world’s biggest, finest diamonds, supported by what Bristow believes is the industry’s sharpest team of diamond valuation and marketing experts, geologists, and a dedicated engineering and operating team, Rockwell has found its own special niche.

The company is strategically positioned at the high end of the value chain. “We don’t mine many diamonds but the ones we do recover are of exceptional value and quickly find buyers. Typically our diamonds sell to private individuals of very high net worth,” reveals Bristow.

The nature of demand is swinging steadily towards the largest, purest gems that are the focus of Rockwell’s operations. In August, Rockwell reported the recovery of five large gemstones from its Holpan, Klipdam and Saxendrift operations. The jewel in the crown was found at Holpan, a massive 136-carat clean white diamond. This brought the total number of stones weighing in excess of 50 carats recovered this year to 11, whereas in the whole of 2009, only a total of 12 gems of this size were found.

The West may be making a slow economic recovery, but China and India are holding up much better. Meteoric growth in some sectors has produced a swathe of new billionaires and millionaires eager to possess the ultimate status symbol. “Even in the West, we see that the highest end of the luxury market has fared better than the sector overall. It is another factor that works in our favour,” Bristow adds.

A successful private placement and rights issue at the beginning of the year raised C$16.9 million, and enabled Rockwell to recapitalise its balance sheet and proceed with the important acquisition and re-development and commissioning of the Tirisano project.

The company is also committed to modernise and re-commission the important Wouterspan operation which is adjacent to Saxendrift in the Middle Orange River area of the Northern Cape Province. Wouterspan was closed due to the negative economic environment in January 2009. The engineering redesign of Wouterspan is almost complete; and project implementation and re-commissioning is scheduled for 2011.

The funds raised early in the year also provided a capital base to support the company in adding to its asset portfolio. “We are not interested in growth for the sake of it,” Bristow asserts. “Rather, we need to be able to create critical mass in terms of production profile and to fully leverage our technical and processing capabilities. It is also important that if maintenance and repair cycles at one mine cause a temporary shut-down, we can continue recovery elsewhere, which acts to smooth revenue flows. We are only interested in acquiring assets with the potential to economically deliver a high grade product and we expect to see a consistent improvement in our recovery rates.”

One acquisition this year has been a 20 per cent stake in Flawless Diamond Trading House, a professional marketing and sales facility which was already used to sell Rockwell's diamond production. However, Bristow is quick to point out that the company has no intention of switching to a vertical integration model.

A further key benefit that Rockwell has in place to leverage off its diamond product is its unique joint venture arrangement with the Steinmetz Diamond Group (SDG), a world leader in terms of the manufacture and marketing of unique and rare large and special diamonds. This partnership ensures that Rockwell attains additional upside in a profit share arrangement that ensures extra margin from the company’s most special diamonds. Typically these diamonds include exceptional coloured stones and product larger than 10 carats which are manufactured, certified and marketed via SDG’s specialised and highly successful diamond business.

“We are deeply committed to focus on our core competence which is alluvial diamond mining. However, in addition to a small revenue stream, what is really important about this acquisition is that it gives us a critical insight into the market, particularly in terms of further penetrating Chinese and Indian markets. We will gain an immediate sense of new trends and changing demands,” he explains.

Looking to the future, Bristow believes that Rockwell will further consolidate its position as a mid-tier supplier over the next five years. “We have resources for at least the next 15 to 20 years and we are adding to these all the time. Then we benefit from a number of committed long-term investors and an improving market environment.

“The basic market fundamentals are excellent,” he continues. “High quality diamonds are becoming scarcer all the time. That fact, combined with the new purchasing power emanating from emerging economies, means that our very high grade output can only become more sought after,” he concludes. www.rockwelldiamonds.com

rockwellDIAMONDS_NOV10_emea_BROCH-s.pdf

rockwellDIAMONDS_NOV10_emea_BROCH-s.pdf