Canadian mining company Mandalay Resources applies the principles of continuous improvement to everything it does. Creating cost-effective and stable operating conditions has enabled the company to reinvest revenue into exploration and develop a long-term pipeline of projects.

With the global financial crisis of 2008, many mineral prices slumped, while gold, always considered a safe bet in hard times, continued to climb in value. In the aftermath of those turbulent times, huge opportunities have arisen for financially and operationally disciplined mining companies to enter the market and establish a significant footprint.

Launched in late 2009 and listed on the Toronto Stock Exchange, Mandalay Resources is one such company. After just two years of focused mine development and production ramp-up, complemented by continuous improvement to reduce operating costs, and an intensive programme of exploration, Mandalay is poised to make the transition to full design production at two of its three mining properties. Meanwhile, efforts to expand significant long-term reserves are well in hand.

“The business is designed around a self-funded strategy: to acquire assets that can be brought to cash flow relatively quickly, and then to reinvest that cash into exploration and growth,” explains CEO Brad Mills. “It’s a stable model—a virtuous cycle—and is paying off handsomely today. This year, we expect to generate $160 million in revenue and approximately $80 million EBITDA [gross profit].”

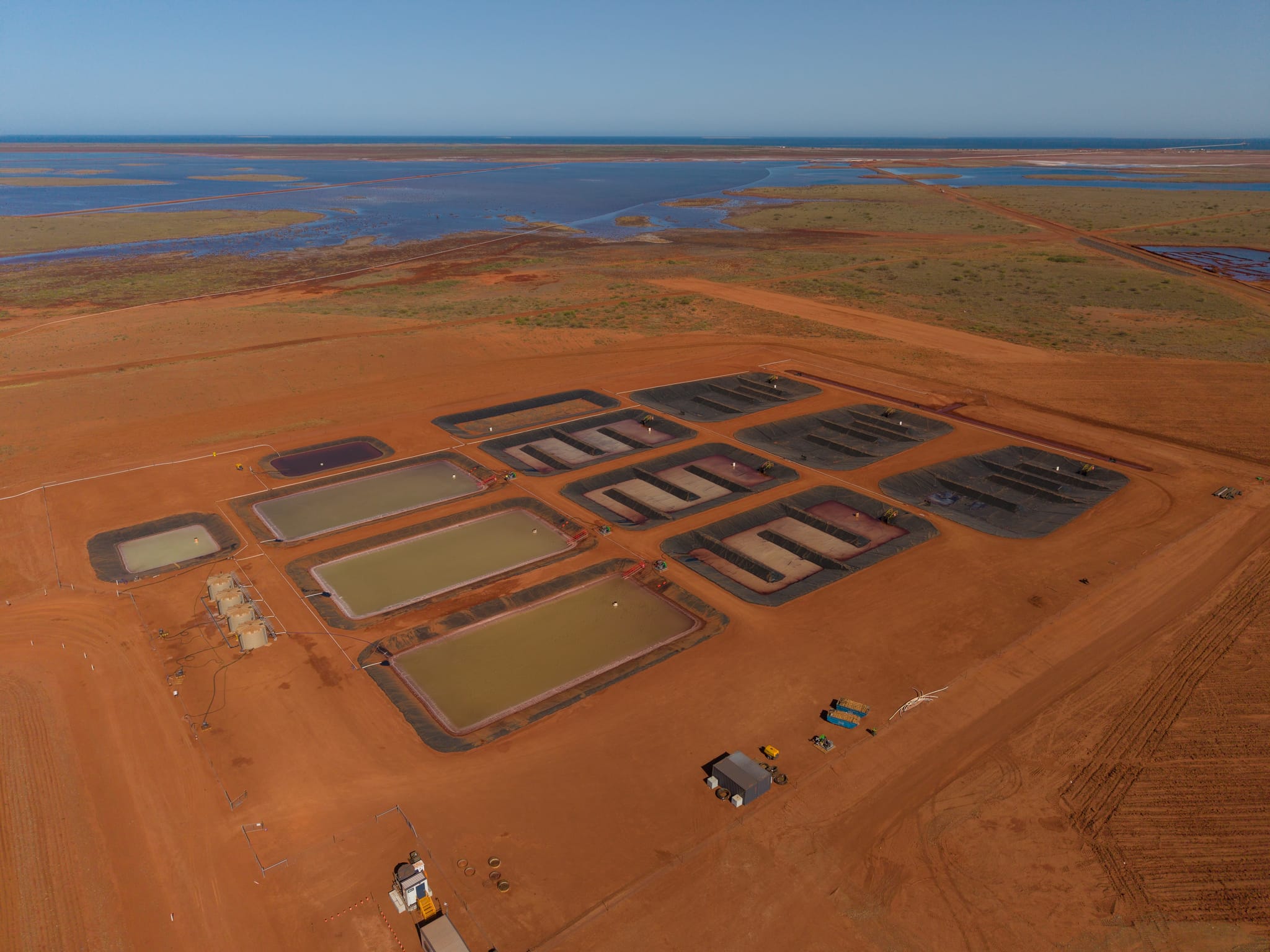

The acquisition trail began with the Costerfield gold/antimony property just 100 kilometres north of Melbourne, Australia. Owned by Western Coal, it had been mothballed during the financial crisis and was quickly brought back into production following the acquisition in December, 2009. Today, Costerfield is producing around 250 tons of high-grade ore a day which is processed on-site to form an antimony-gold concentrate typically containing 55 per cent antimony and around 100 grams per ton of gold. The concentrate is then shipped and sold to smelters in China.

Bringing the existing mine back into operation was initially a matter of reinstating the existing mine plan and rehiring staff. Reaching a cost effective and stable operating status, however, required considerable investment and change. “We had to address a large suite of operational issues,” Mills says. “The original design was for an open-stope mine, but we ran into problems with rock mechanics and stability in the open stopes, and we were getting a lot of dilution. So we couldn’t deliver the quality or tonnage of ore that we wanted.”

This is where the company’s in-house expertise in continuous improvement came to the forefront. After trialling several innovations to the mining method the best solution was found to be a technique called ‘cemented rock backfill’ that was implemented during the second half of last year. “This resolved our grade and tonnage issues, and we’re now operating at 25 per cent above the plan design,” says Mills. With production stability now established, the focus has shifted to continuously improving performance reliability and cost efficiency.

Costerfield has significant prospects for the future. The property extends the full seven kilometre length of the known mineralisation in the district. “At the time we bought the mine it only had about one year’s worth of reserves, but we believed there was a million ounces of gold here somewhere. We started exploration about a year ago, and have been able to replace reserves each year. However, at the end of last year we made a major new discovery at the Cuffley lode,” Mills continues.

Exploration efforts elsewhere on the property were suspended. Attention focused purely on the Cuffley discovery, and the results look very promising. “At this stage it looks as though we will be able to extend the mine life to between seven and 10 years and expand production by 50 per cent to maybe 350 or 400 tons a day,” says Mills. The long-term mine plan for Costerfield is currently being rewritten and will be published later this year, when the future of Cuffley will be decided. However, an early estimate suggests that an investment of around $15 million will be required over a period of 12 to 18 months to construct the new mine, ramp it up to production, and concurrently expand the Costerfield grinding mill and flotation plant capacity to handle the increased throughput.

If all goes according to plan, Costerfield will then produce 40,000 ounces of gold and 5,000 tons of antimony annually, generating revenue of around $100 million, and a 50 per cent margin.

The second major acquisition, the Cerro Bayo silver and gold mine in southern Chile, took place in September, 2010. Mined for some 10 years by Coeur d’Alene Mines Corporation, it was closed during the financial crisis due to a combination of high operating costs and limited reserve life. However, new reserves have been discovered on-site.

Mandalay’s approach to Cerro Bayo has three facets. Firstly, three new mines are at various stages of development and production and they feed directly into the existing plant, producing a gold-silver concentrate with an average grade of 11,500 grams silver and 70 grams gold per tonne. The Fabioloa mine and the Dagny mine are both up and running and deliver 400 tons of ore a day each, while the Delia mine is currently ramping up to a similar level of production by the fourth quarter of 2012.

Meanwhile, Mandalay has fully mechanised the mining process in these three mines, and has thereby been able to significantly reduce operating costs. “The Cerro Bayo plant has an installed capacity of 1,600 tons a day,” Mills explains. “Coeur was employing 1,000 people to deliver that. By mechanising the mining process, we are producing 1,200 tons of ore a day with just 400 people, so we have a very different cost footprint which makes us a lot more competitive.”

Finally, Mandalay has a clearly defined and ongoing programme of exploration to exploit the huge potential at Cerro Bayo. The property is very large, measuring some 25 kilometres by 10 kilometres, and contains hundreds of known veins. “We believe the overall potential here is in excess of 100 million ounces,” says Mills. By the end of the first year of exploration, the two-year mine life had been extended to five years. “And we expect to double that again this year. This will then allow us to open a fourth mine, Delia South East, taking us up to our full operating potential of 1,600 tons of ore a day. At that point Cerro Bayo will be producing around five million ounces of silver and 50,000 ounces of gold a year.” The timescales for development of Delia South East will be defined later this year.

Mandalay does have a third property in its portfolio, a copper-silver project, but this is at a much earlier stage of exploration. Located in northern Chile, La Quebrada was part of the original Mandalay Resources Corporation portfolio before the current management team took it over. The results of the first two years of detailed exploration are shortly to be released with an initial estimate of the mineral resources that will form the basis for a longer term strategy for the property.

Mandalay’s strategy is based on investing $15 million to $20 million per year on exploration to ensure a long pipeline of reserves for future development, and that level of investment looks set to continue. Operationally, stability and financial strength have been achieved through a combination of continuous improvement to reduce costs and improve productivity, and rigorous data analysis to monitor performance against targets. “We aim for stability and consistency. Once we get those, we can move to a higher level of performance,” Mills concludes.

Written by Gay Sutton; research by Dan Finn

DOWNLOAD

Mandalay-EMEA-July12-Bro-s.pdf

Mandalay-EMEA-July12-Bro-s.pdf